A Total Eclipse of the Market

A Total Eclipse of the Market

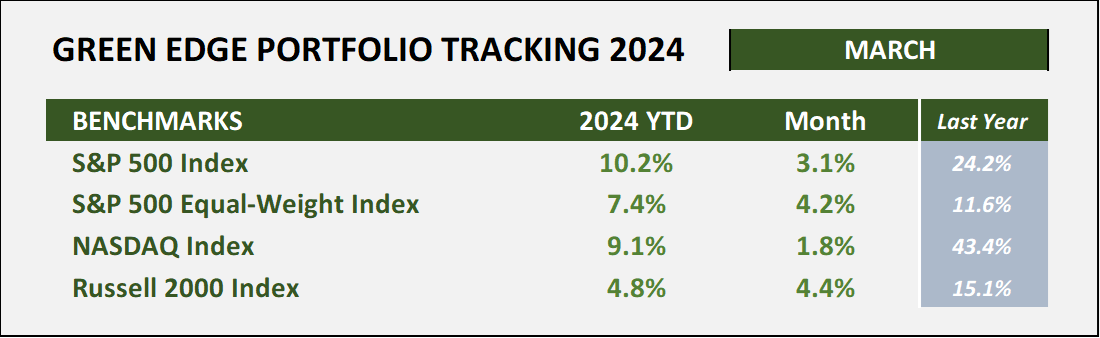

March 2024 Portfolio Performance results

Yesterday’s total eclipse was an amazing event. No, I didn’t drive four hours to get into the totality zone but did experience temperature dropping by almost 10 degrees and a strange darkness in the middle of the afternoon. Plus, we were able to catch a Vampire Weekend concert as they kicked off their musical tour at noon on Total Eclipse Day from Austin, TX. They will be in Milwaukee on August 1st, if you are a fan. But what’s most important is that the World got through the ordeal, and we still all exist, much to the demise of the clairvoyants that called for the end of the world.

It reminds me of the perma-Bears who continuously tell us that the end of the bull market is upon us and to be ready for 50%+ drawdowns. They point to inflation or high interest rates or the unprecedented level of U.S. debt or global wars or an asteroid is going hit us. There is always something to be afraid of.

Living in a place of fear is not healthy and keeps us from achieving all that life has to offer. Therefore, I feel sorry for the doomers. So, we push forward, maybe with a bit of healthy skepticism, but optimistic to the world, the markets, and opportunities around us. Let’s Go!

General Market Commentary

What do you notice about the monthly performance? Your right! The equal-weight +4.2% and the small cap index +4.4% beat out the S&P500 +3.1% and NASDAQ 1.8% in a positive direction. The bull market is broadening out, at least for one month, and this is good. The S&P equal weight still trails the S&P500 YTD by almost 3% (+7.4% vs +10.2%) but picked up +1.1% in March.

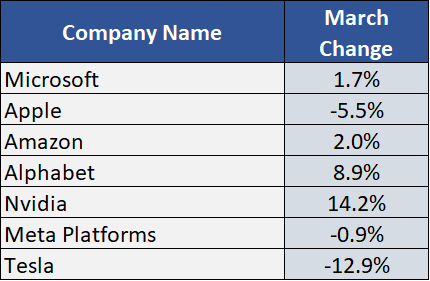

The Magnificent 7, for once, did not lead the market higher. Well, maybe Nvidia still had a good month but, in total, the average appreciation was just over +1% with Apple and Tesla being the weakest. These seven stocks still make up 29.1% of the market cap of the whole 500 companies included in the S&P500 index.

Last month I mentioned positioning my portfolio for a 5-10% correction but suggested that you shouldn’t try this at home. And I was right. It was stupid to not continue to be fully invested in this bull run. On March 1st, I was 25% cash and 10% in a leveraged short on the NASDAQ (SQQQ). I waited for bad news on the Consumer Price Index (CPI). Waited for bad news on the Producer Price Index (PPI). Both were a little hot, but the market shook it off and continued higher. Waited for Fed Chairman Powell’s hawkish commentary during the Fed meeting. Didn’t happen. He basically said that a strong labor market wouldn’t prevent the Fed from lowering interest rates. Boom. Stocks took off and I re-positioned back for all out bullish action again. Sold the SQQQs and deployed cash back down to ~10% cash position. I hated “cheering” for bad news anyway. I’m not very good at being a Bear. Eventually we will get a correction as it happens periodically in every bull and its good for the market to rest.

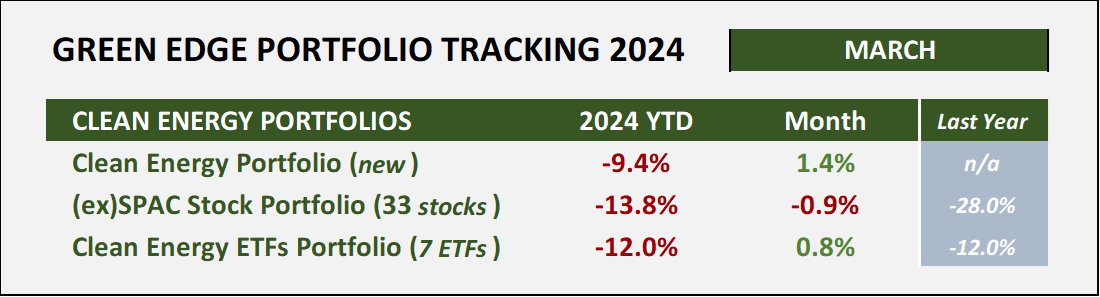

Clean Energy Performance Tracking Table

Clean energy stocks trailed the major indexes in March with the basket of ETFs up +0.8% versus the +3.1% on the broad S&P500 index. Our SPAC portfolio, made up of 33 companies that came public through SPACs, was down on the month -0.9%.

You can follow this portfolio on Savvy Trader for free.

Top stock of the month: NuScale Power (SMR), up +71.3% for the month. After hitting a low of $1.88 in mid-January, SMR rallied to as high a $11.21 on March 18th for a 500% increase from the bottom. The move up was a direct result of an investor update that the company’s small nuclear reactor plant in Romania received a $4 billion commitment from the U.S. Government. This would effectively become “Europe’s first project using the technology” paving the way for greater adoption and a longer-term growth profile. SMR closed the month at $5.31. This company remains very far away for a profitable quarter.

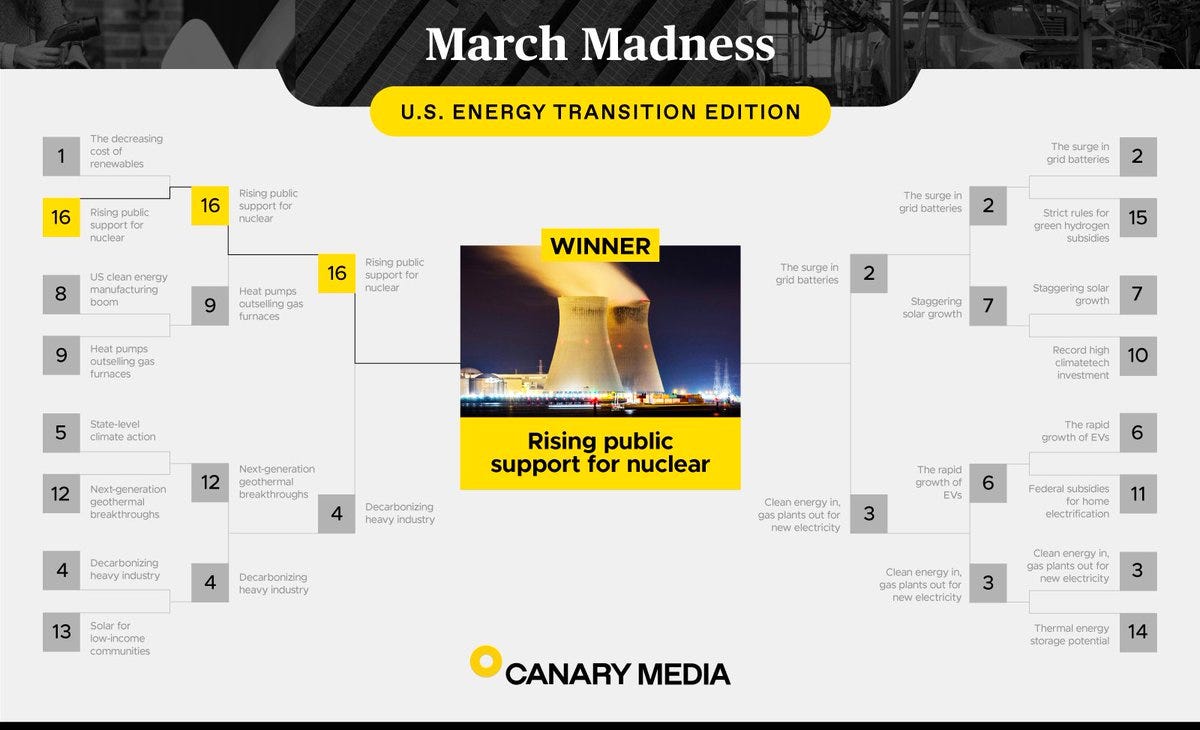

Whether you are a fan of nuclear power or not, there has been a renaissance of sorts on the technology and bipartisan support where there hadn’t been in the past. A quick story which shows this support is a March Madness contest for U.S. Energy Transition Edition created by Canary Media. They had clean energy folks select and rank the top technologies to make it into the top 16 and them put them in order. Number 1 faced off against number 16, 2 versus 15 and so on. Nuclear barely made it into the contest at the #16 seed. In round one, it pulled an upset over #1 (The decreasing cost of renewables). The voting took place on X (Twitter). Check out who won the tournament in the bracket results below:

Yes, “Rising public support for nuclear”. Check out the X post here: Canary Media Sweet 16 Clean Energy Playoffs

In other news, electric vehicle maker Fisker (FSR) began to explore bankruptcy filing in March. It was only in September of 2023 that its stock was trading at $7/share. Today, in the over-the-counter market, it trades at $0.02/share. Talks with a large automaker faltered and they are currently evaluating ways to save the company. In the meantime, Fisker has reduced the MSRP price on its EVs by 30-40%. For example, the 2023 Ocean Extreme price was lowered to $37,499 from $61,499, or a drop of 39%. Just in case you want to pick up a cheap EV.

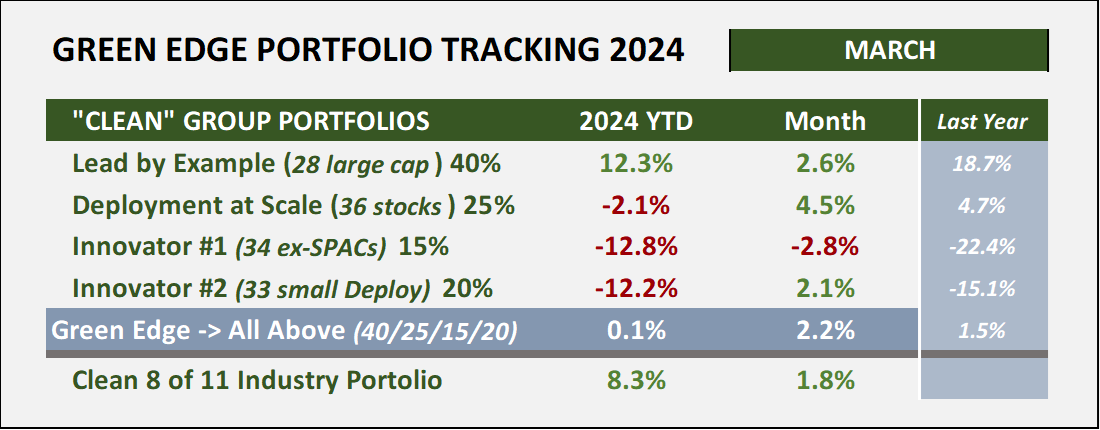

Quick update on the Clean Group portfolios. YTD innovator groups continue to drag on the full portfolio, although it did make it out of the red and into the green by +0.1%. The large cap “Lead by Example” group of 28 companies taking action on sustainability are beating the S&P500 YTD +12.3% vs. +10.2%, so it seems to be good business to be good for the environment. See the performance table below.

In the 8 of 11 industry portfolio, its +8.3% rise trails the S&P500 performance after March activity as the energy sector had a good month on higher oil prices, up +9.6% for the month.

Cryptocurrency Portfolio

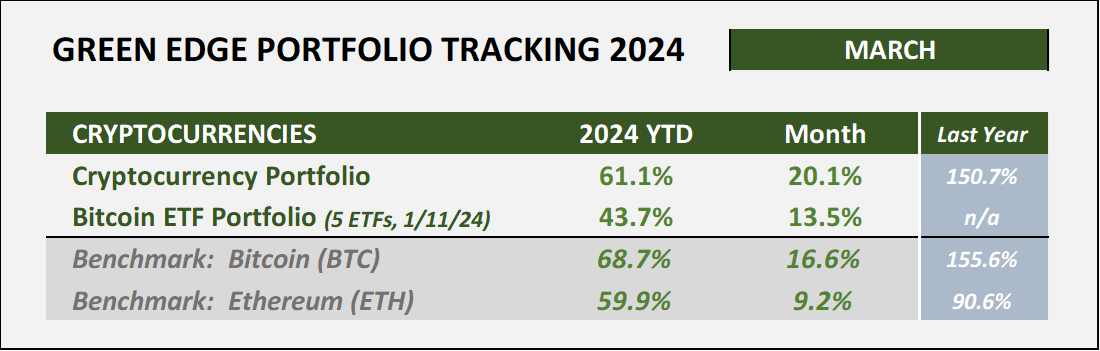

Bitcoin rose +16.6% in March while Ethereum was up +9.2%, however the whole crypto portfolio rocketed +20.1%. Dogecoin (DOGE) and Solana (SOL) were the stars of the month appreciating 88% and 61%, respectively. SOL has doubled YTD and DOGE is up +145%.

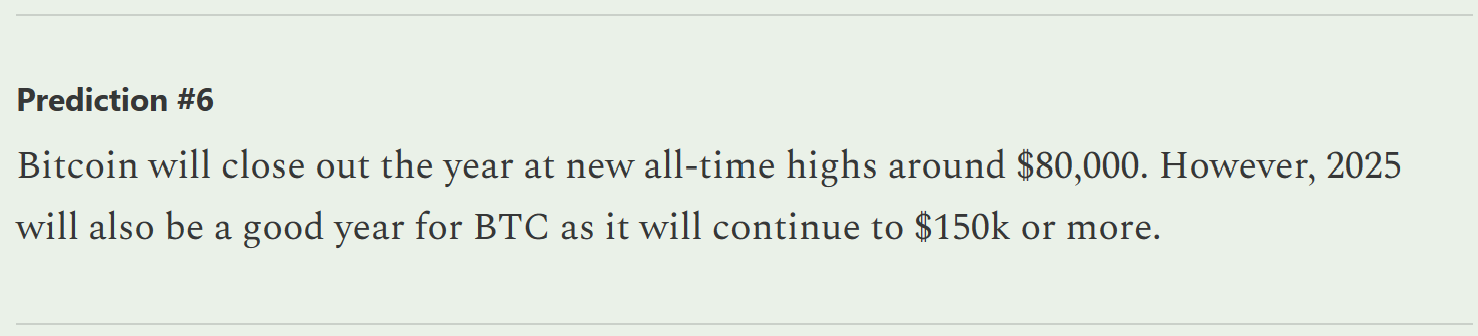

The Bitcoin halving will happen in the month of April. The new ‘inflation’ rate of total Bitcoin being produced will drop in half from ~1.7% down to ~0.85%, or less than 1% per year. With the advent of the Bitcoin ETFs, there is not enough Bitcoin being produced to satisfy the demand. This is, and will continue to, result in higher BTC prices. During this four-year cycle, ‘experts’ are calling for BTC price to increase to over $100,000 with some forecasting $150,000, $200,000 and even up to $300,000 in 2025. In my 2024 prediction edition, I suggested $150,000 top, but only $80,000 in 2024.

If I could change my 2024 estimate, it would increase by $20-40k. History of the 4-year cycle shows that Bitcoin prices peak about 12 months after the halving but then can retrace 75% or more in the cycle.

Thank you for your support and reading this edition. Let me know if you have any comments or questions. And <Like> this edition if you have a chance. Thank you and have a wonderful April.

Efficiently Yours,

D.T.