Up for the Challenge

Up for the Challenge

May Portfolio Update: clean energy, SPACs, NFTs, crypto, social tokens

"What seems challenging now will someday be your warm-up." - Unknown

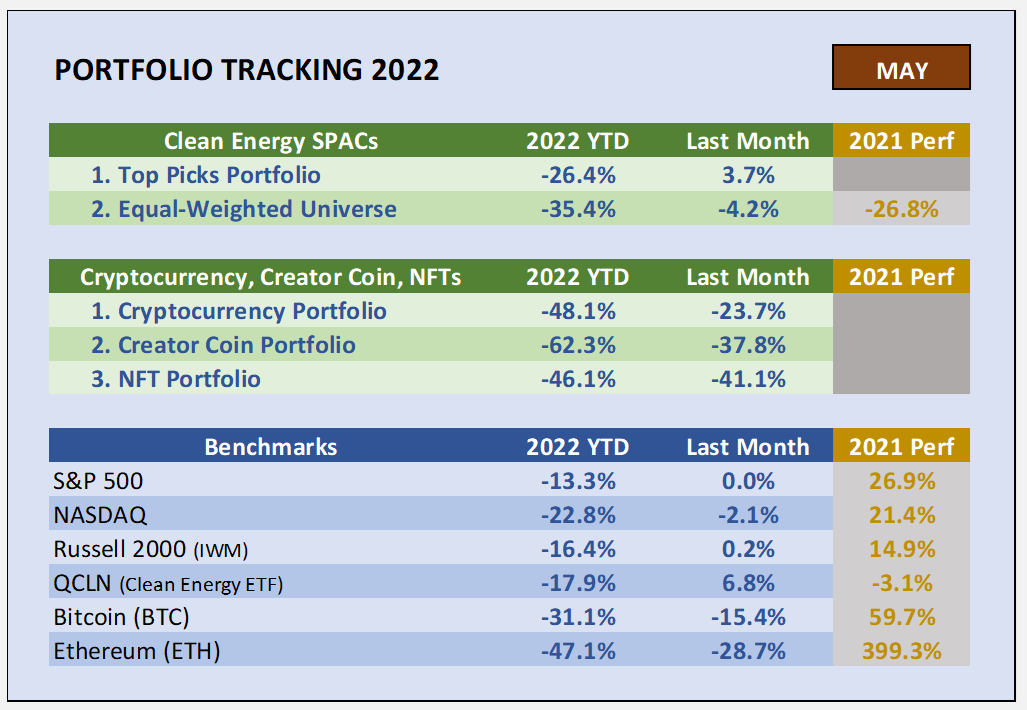

Portfolio Performance Update

I sure hope we can look back at the challenging first five months of 2022 and believe it was just a warm-up for the bulls to come back into game and rally by the end of the year. I know this is not a good interpretation of the quote, so I do dive in a bit more later in this edition. On to the analysis…

The S&P 500 index hit a new 52-week low on May 20th but bounced back hard in the last week to finish essentially even for the month, up 0.005%. The tech heavy NASDAQ finished down 2.1% while the small company-based Russell 2000 and the Clean Energy ETF were green for the month, up 0.2% and 6.8%, respectively.

With clean energy up nicely for the month, it carried forward in our Top Picks portfolio which gained 3.7%. This compared positively to the equal-weighted portfolio which lost 4.2% in May and now holds a 9% advantage YTD, even though both are down significantly for the year: -26.4% vs -35.4%.

Cryptocurrency market experienced further bear price action in May with Bitcoin (BTC) down over 15% and Ethereum (ETH) down a whopping 28.7%. Since mid-November 2021 highs, BTC is off about 54% and ETH 60%.

Don’t forget to subscribe to get this newsletter in your in-box each month.

Sell in May and go away?

From 1950 to 2020, the average gain for the six months of the year from May 1 to Oct 31 is only 0.8% per year. However, the other six months of the year (from Nov 1 to Apr 30), the average annual return is 7.5%. Hence, the saying, “Sell in May and go away”.

How is it working this year? Well, from 11/1/21 to 4/30/22 the S&P500 was down 10.1%, 17.6 points off the average return for the “good” six months of the year. As we indicated earlier, month one of the “bad” six months (May 2022) performed at breakeven. It begs the question, should we have sold on May 1st and forgot about the market until Halloween? Since it was even for May, we can still sell. And what the hell is in store for us during the next five months?

The Fear-Greed Index hit the extreme fear category in late May, and it seems that everyone believes we are in for one more leg to the downside. Take 1: If everyone is leaning to one opinion (going lower), maybe it doesn’t happen: hence, we’ve seen the lows of this correction. Take 2: Or maybe recession is upon us, and we have a longer-term bear market ahead. Me: I’m an optimist, so I expect that not selling on May 1st (or now) is a good idea. Time will tell.

In the meantime, I’m an advocate for dollar-cost averaging, especially for those of you early in your careers - 20’s or 30’s. If you got a late start on investing (i.e., in your 40’s or 50’s), you may need to step up on the monthly contributions. Here is the investment thesis, strategy, and benefit as a reminder. For the last 100 years, the market has always come back to make new highs.

Overall Investment Thesis: The market will be higher in the long-term.

Strategy: Dollar Cost Averaging (DCA) which is investing a small amount every week/paycheck/month into an index fund.

Benefit: Less worry (no FOMO or FUD), less personal time commitment, and use the advantage of time to compound your returns in the long run.

The S&P500 Index charted since 1927 on the log scale, not adjusted for inflation.

Clean Energy Portfolios

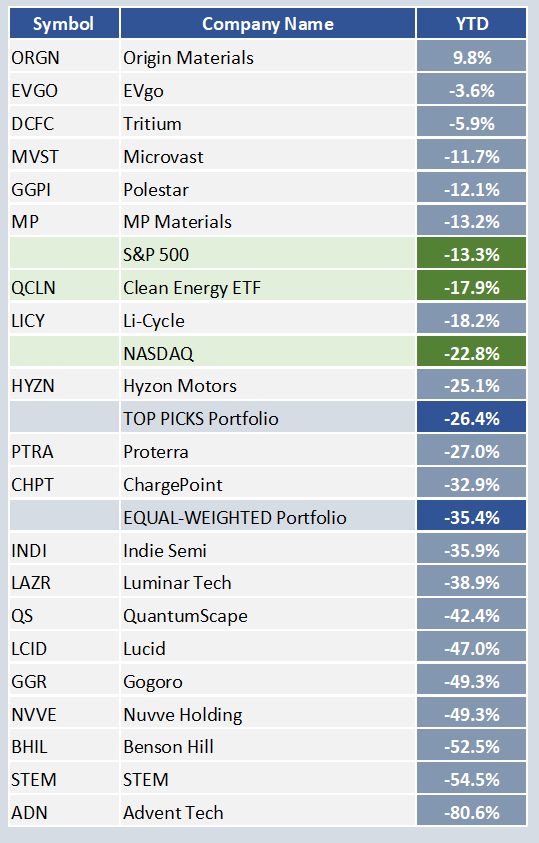

The Top Picks portfolio beat the Equal-Weighted Portfolio in May by 7+ points and now leads by 9% YTD. I thought it would be interesting to show the YTD returns of individual stocks in the Top Picks portfolio and compare to the benchmarks. There is only one stock in positive territory for the year, Origin Materials which has gained 9.8%. Six of the 19 have performed better than the S&P500, but five have lost 49% or more.

Note that two stocks were acquired after 1/1/22, so the Top Picks portfolio fared better than the YTD percentage on those two, Tritium (DCFC) and Gogoro (GGR) => both electric charging firms. The cost basis of these two most recently de-SPACed companies is $7.29 and $5.84 versus the 1/1/22 prices of $9.97 and $9.88, respectively. I had waited for the post de-SPACing drop to pick up the shares for the portfolio. From entry prices, DCFC is up 18% and GGR is down 6%. In addition to DCFC and GGR, EVgo (EVGO) and ChargePoint (CHPT) were the first two electric vehicle charging companies. I went into 2022 knowing that the EV charging sector would be a higher growth area in the near future, so overweighted with these four strong competitors.

The worst performer to date, Advent Technologies (ADN), was a last minute add to the portfolio because I wanted more exposure to hydrogen sector (Hyzon was my top pick). It is apparent that we are much too early for hydrogen powered transportation as the infrastructure in nascent. This is likely a second half of the decade (or next decade) thing. I will likely offload ADN in the next couple of months by selling into any strength. ADN was a smaller position (about 2.9% of portfolio) due to the risker nature of the company.

Here is the Clean Energy SPAC investment thesis to ensure we all know why I’m writing this damn newsletter. <smiley face>

Sector Investment Thesis: The 2020’s decade will experience a significant energy transition to a clean energy economy providing outsized returns to innovative companies in the clean energy space.

Strategy: Invest in clean energy companies coming public through SPACs, de-SPACed or announced, by 12/31/2021. Set up two portfolios for tracking: 1) Equal investment into all 75 companies, and 2) Invest in what I consider the top 25% for the Top Picks.

Cryptocurrencies, NFTs, and Social Tokens

As the stock market’s rallied into the end of the month to finish even, the crypto market diverged lower with BTC losing 15.4% and ETH down 28.7%. Year-to-date ETH has lost 16% more than BTC leading the BTC Dominance to gain four (4) percentage points in May alone going from 42.7% up to 46.7%. BTC Dominance is the percentage of BTC market cap to the total cap of the whole cryptocurrency market.

BTC Dominance shrunk in 2021 from a high of over 73% in January to a low of about 39% in January of 2022 (see chart above). It was a strong year of performance for most alt-coins. However, in the last few months, BTC has been stronger in a down market (losing less than alternative coins) as dominance has grown to nearly 47% and seems posed to continue its gains in the near future; likely to exceed 50% before alt-coins could potentially recover (maybe hit 56-57%?). The crypto bear market of 2018 lasted about one year where BTC fell 84% and ETH down 90%. Of course, the 18-month bull market that followed in experienced crazy returns of 1700% and 5300%, respectively.

Since NFTs and Social Tokens are strongly tied to crypto markets, it is of no surprise that these markets are significantly lower as investors fled to Bitcoin, stable coins, or cash. However, there are winners in the space as what matters to projects is the value of the utility that comes from holding an NFT or social token.

For example, on the Rally network, social tokens are based on value to Rally coin (RLY). The ADHD coin appreciated 100% in May from 30 RLY to 1 ADHD up to 60-1. Since RLY moved down over 50% in May, the ADHD token remainder at about the same USD price. This token Superpowers the NFT365 daily podcast and mints a new NFT each day for 365 days.

Another example in an NFT project is the Giraffe Tower. At the end of April, this project had a floor price of about 0.06 ETH and today it has more than doubled to 0.13. This community attracts 40-75 people each morning for discussion over coffee, but only for holders of a Giraffe. And creators who hold 25 Giraffes have free beta access to Social Connector, a technology system for creators.

NOTE: I do own tokens and NFTs in both of these communities.

Building on the Quote (at the top of the page)

"What seems challenging now will someday be your warm-up." - Unknown

The book, Smart Growth: How to Grow Your People to Grow Your Company by Whitney Johnson, came to mind when I first saw this quote from “Unknown”. Ms. Johnson describes the “S-Curve of Learning” in her book on how one experiences the journey of taking on a new field or subject (see the graphic below for a map of this journey).

Link: McKinsey Interview Article with Whitney

As one takes on a new field/job/role, you start on the left side of the chart in the launch stage and move through to building competence, confidence, and then to mastery. It’s an awesome achievement to reach the Mastery level in your role where you can feel confident in your knowledge and the ability to perform at a high level. You become an expert in your field.

But it is our nature to want to explore and experience growth. The excitement of starting a new thing. That feeling doesn’t necessarily happen at the Mastery level. The growth comes from exploring new areas and learning new skills. The concept also feels in alignment to our portfolio approach. It makes sense to have some subjects where you are in mastery and have others in the exploratory phase. A good portfolio of subjects/fields provides you with the responsibilities where you can be an expert but also areas to feed into your growth aspirations.

Six months ago, I started exploring the technology change we are experiencing. With blockchain as the foundational technology, it allows for the growth of what people are referring to as “Web3” which includes components such as crypto, NFTs, social tokens, and the metaverse. One day soon, I’ll write up an edition of this newsletter that will provide my take on Web3 and how it may change business models in the future. Until then, good luck in the markets.